When the EU Deforestation Regulation came into force, it covered seven commodity groups: cattle, cocoa, coffee, palm oil, soy, wood, and rubber. The compliance framework is the same for all of them — Due Diligence Statements, geo-coordinates, risk assessment, operator responsibility.

But the upstream data reality is very different depending on which commodity you are importing.

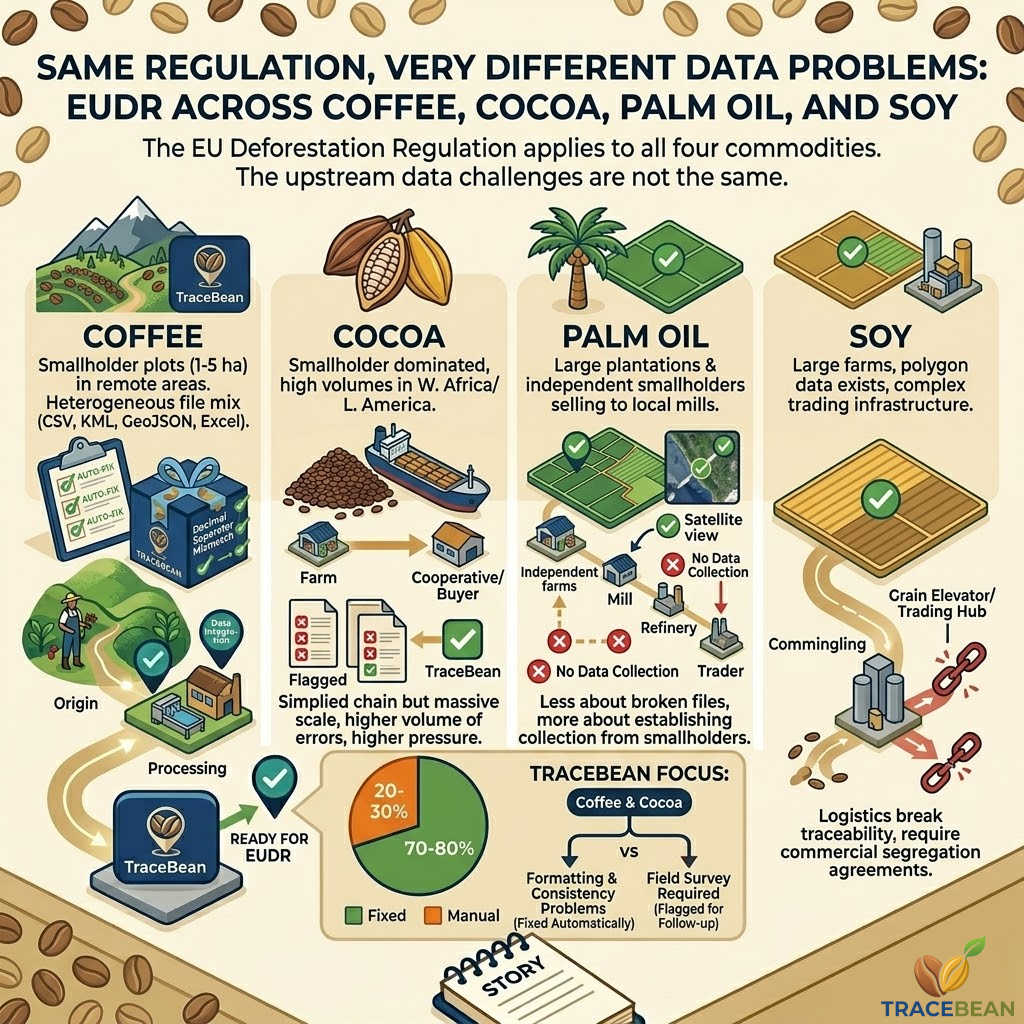

Here is what we see across the four main agricultural commodities.

Coffee

Coffee

Coffee is where TraceBean started, and for good reason. The upstream data problem in coffee is well-defined and consistent.

Most green coffee is grown by smallholder farmers — plots of one to five hectares, often in remote mountain areas with limited digital infrastructure. Suppliers collect farm data using mobile apps, GPS devices, or paper forms that are later digitised. The result is a heterogeneous mix of formats: CSV exports from local databases, KML files from Google Earth, GeoJSON from NGO-supplied tools, Excel spreadsheets built by hand.

The errors are predictable: decimal separators, swapped coordinates, empty farm ID fields, non-standard tags, point geometry where polygon is required. Around 70–80% are auto-correctable. The rest require field follow-up.

The traceability chain in coffee also has a specific complexity: the washing station. In wet-processed origins — Ethiopia, Kenya, Colombia — multiple smallholder farms deliver cherry to a central processing station. The shipment is traceable to the station, but tracing it back to individual farms requires linking station records to farm geo-data. This is a data integration problem, not just a data quality problem.

Cocoa

Cocoa

Cocoa shares many characteristics with coffee. Smallholder dominated, West Africa and Latin America as primary origins, mobile data collection with variable quality.

The key difference is scale. The cocoa supply chain is concentrated in Côte d'Ivoire and Ghana, which together produce around 60% of global supply. These two countries have millions of registered smallholder farmers — numbers that dwarf the coffee sector. At that scale, even a small error rate produces enormous volumes of flagged records.

There is also no washing station equivalent in cocoa — traceability goes directly from farm to cooperative or buyer. This simplifies the chain but makes farm-level data quality even more critical, since there is no intermediate aggregation point to absorb inconsistencies.

The data quality pattern is similar to coffee: coordinate errors, missing polygons, inconsistent IDs. The volume is higher. The pressure from major chocolate manufacturers — who have been working on traceability longer than the coffee sector — means some supplier datasets are more mature, but coverage is still far from complete.

Palm Oil

Palm Oil

Palm oil presents a structurally different problem.

Large plantations — hundreds or thousands of hectares — are common among major producers in Indonesia and Malaysia. For these, polygon data exists, satellite imagery is available, and the geo-data is often already in usable formats. The large operators have been under traceability pressure from consumer goods companies for years.

The problem is at the other end: independent smallholders who sell to local mills, which then sell to refiners, which then sell to traders. By the time palm oil reaches a European importer, it has passed through multiple hands and the farm-level traceability has often been lost. The data gap is not a formatting problem — it is a supply chain structure problem. Rebuilding traceability requires going back several steps in the chain.

The upstream data quality issue for palm oil is therefore less about fixing broken files and more about establishing data collection where none exists.

Soy

Soy

Soy is the most structurally complex of the four.

Brazilian and Argentine soy farms are large — thousands of hectares — and polygon data generally exists for registered properties. The geo-data quality at farm level is often better than in the other commodities.

The challenge is the trading infrastructure. Soy passes through grain elevators and trading hubs where it is commingled with soy from multiple origins and multiple farms. By the time it reaches a European port, the farm-level traceability has been broken by the logistics chain, not by data quality problems. Reconstructing it requires source segregation agreements and documented chain of custody — a commercial and contractual challenge more than a data one.

What this means for TraceBean

TraceBean is currently focused on coffee and cocoa — the two commodities where the upstream data problem is a formatting and consistency problem that automated validation and correction can address directly. Palm oil and soy present structural supply chain challenges that require different solutions.

The EUDR regulation is the same for all four. The work required to comply with it is not.

Clean data in, clean DDS out. The upstream step is where compliance is won or lost — and it looks very different depending on what you are importing.